All Categories

Featured

Table of Contents

There is no payment if the plan expires prior to your fatality or you live beyond the plan term. You might have the ability to renew a term policy at expiry, yet the costs will certainly be recalculated based on your age at the time of renewal. Term life insurance policy is generally the the very least expensive life insurance policy readily available because it uses a fatality advantage for a restricted time and doesn't have a cash value element like irreversible insurance coverage.

At age 50, the premium would certainly rise to $67 a month. Term Life Insurance Policy Fees 30 years old $18 $15 40 years of ages $28 $23 50 years old $67 $51 Resource: Quotacy. Quotes are for a $250,000 30-year term life policy, for guys and females in excellent health and wellness. On the other hand, here's an appearance at prices for a $100,000 whole life policy (which is a sort of irreversible policy, indicating it lasts your lifetime and includes money value).

The reduced danger is one element that permits insurers to charge reduced costs. Rate of interest rates, the financials of the insurance policy company, and state policies can additionally influence costs. As a whole, firms usually supply better prices at the "breakpoint" coverage degrees of $100,000, $250,000, $500,000, and $1,000,000. When you consider the amount of protection you can get for your premium bucks, term life insurance policy often tends to be the least pricey life insurance.

Thirty-year-old George wants to secure his household in the unlikely occasion of his sudden death. He gets a 10-year, $500,000 term life insurance policy plan with a costs of $50 per month. If George passes away within the 10-year term, the policy will pay George's recipient $500,000. If he dies after the plan has ended, his recipient will certainly obtain no benefit.

If George is diagnosed with a terminal illness throughout the very first policy term, he possibly will not be eligible to renew the policy when it expires. Some plans use guaranteed re-insurability (without evidence of insurability), yet such functions come with a higher expense. There are a number of sorts of term life insurance policy.

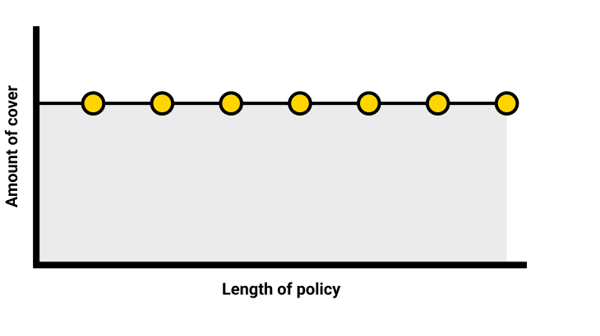

The majority of term life insurance has a level premium, and it's the type we have actually been referring to in most of this article.

Budget-Friendly What Is Voluntary Term Life Insurance

Term life insurance policy is eye-catching to young people with youngsters. Parents can acquire considerable protection for an inexpensive, and if the insured dies while the policy holds, the family members can rely upon the death benefit to change lost earnings. These plans are also fit for individuals with growing family members.

The best selection for you will depend on your demands. Here are some points to think about. Term life plans are suitable for individuals that desire significant coverage at an inexpensive. Individuals that possess whole life insurance policy pay much more in premiums for less coverage however have the security of knowing they are secured forever.

The conversion cyclist need to enable you to convert to any irreversible policy the insurance business provides without limitations. The main features of the biker are keeping the original health and wellness ranking of the term plan upon conversion (also if you later on have health issues or come to be uninsurable) and choosing when and just how much of the coverage to transform.

Naturally, overall premiums will certainly enhance considerably considering that whole life insurance policy is a lot more pricey than term life insurance policy. The benefit is the ensured approval without a medical examination. Clinical conditions that establish during the term life duration can not create costs to be enhanced. However, the business might require restricted or full underwriting if you want to include added bikers to the brand-new plan, such as a long-term treatment rider.

Entire life insurance coverage comes with considerably higher month-to-month costs. It is implied to supply protection for as lengthy as you live.

Value Level Premium Term Life Insurance Policies

Insurance policy firms established a maximum age limitation for term life insurance policy plans. The premium also climbs with age, so an individual aged 60 or 70 will certainly pay substantially more than somebody decades more youthful.

Term life is somewhat comparable to cars and truck insurance policy. It's statistically not likely that you'll require it, and the costs are cash down the tubes if you do not. Yet if the worst occurs, your household will receive the benefits.

The most preferred kind is now 20-year term. Many firms will certainly not offer term insurance policy to a candidate for a term that ends past his or her 80th birthday. If a plan is "renewable," that implies it continues effective for an added term or terms, as much as a defined age, also if the health of the insured (or various other elements) would cause him or her to be turned down if he or she made an application for a brand-new life insurance coverage policy.

So, premiums for 5-year eco-friendly term can be degree for 5 years, after that to a new price reflecting the brand-new age of the guaranteed, and so on every 5 years. Some longer term policies will certainly guarantee that the costs will not raise during the term; others do not make that guarantee, making it possible for the insurance provider to increase the price during the policy's term.

This indicates that the plan's owner has the right to transform it right into a long-term kind of life insurance coverage without added proof of insurability. In a lot of kinds of term insurance policy, consisting of house owners and car insurance coverage, if you have not had a claim under the policy by the time it runs out, you obtain no refund of the costs.

Level Term Life Insurance Definition

Some term life insurance coverage consumers have actually been dissatisfied at this outcome, so some insurance firms have actually created term life with a "return of premium" feature. annual renewable term life insurance. The premiums for the insurance policy with this function are frequently dramatically greater than for plans without it, and they generally call for that you keep the plan effective to its term otherwise you waive the return of premium advantage

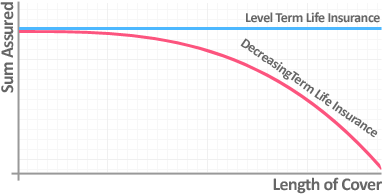

Degree term life insurance policy costs and death benefits stay consistent throughout the policy term. Degree term life insurance policy is generally more cost effective as it does not develop money worth.

Trusted Does Term Life Insurance Cover Accidental Death

While the names frequently are utilized reciprocally, degree term protection has some important differences: the costs and fatality advantage remain the exact same throughout of protection. Level term is a life insurance policy policy where the life insurance policy costs and survivor benefit stay the same throughout of insurance coverage.

{kind=link}

Table of Contents

Latest Posts

Senior Care Funeral Insurance

Funeral Cover Benefits

Burial Insurance Prices

More

Latest Posts

Senior Care Funeral Insurance

Funeral Cover Benefits

Burial Insurance Prices