All Categories

Featured

Table of Contents

That usually makes them an extra economical option for life insurance protection. Many individuals get life insurance policy coverage to aid financially secure their loved ones in instance of their unforeseen death.

Or you may have the choice to convert your existing term insurance coverage into a permanent plan that lasts the remainder of your life. Different life insurance policy plans have prospective advantages and disadvantages, so it is essential to comprehend each prior to you choose to acquire a policy. There are several benefits of term life insurance policy, making it a prominent selection for coverage.

As long as you pay the costs, your recipients will certainly get the survivor benefit if you pass away while covered. That claimed, it's essential to note that many plans are contestable for two years which means protection might be retracted on fatality, should a misstatement be located in the application. Plans that are not contestable typically have a rated survivor benefit.

Costs are typically less than whole life plans. With a degree term policy, you can select your protection quantity and the plan length. You're not locked into an agreement for the rest of your life. Throughout your policy, you never need to stress concerning the premium or survivor benefit quantities changing.

And you can't cash out your policy throughout its term, so you will not get any financial advantage from your past coverage. Similar to other sorts of life insurance, the price of a level term plan relies on your age, protection requirements, work, way of life and health and wellness. Generally, you'll discover extra budget friendly coverage if you're more youthful, healthier and less dangerous to insure.

Guaranteed Level Term Life Insurance Meaning

Since level term premiums remain the very same for the period of coverage, you'll understand precisely just how much you'll pay each time. That can be a huge aid when budgeting your expenditures. Degree term protection additionally has some versatility, allowing you to personalize your plan with extra attributes. These typically been available in the kind of motorcyclists.

You may need to meet specific conditions and credentials for your insurance provider to establish this motorcyclist. Furthermore, there may be a waiting period of up to six months prior to taking result. There also could be an age or time frame on the coverage. You can include a youngster rider to your life insurance plan so it additionally covers your kids.

The death benefit is typically smaller sized, and protection usually lasts till your youngster transforms 18 or 25. This rider may be an extra economical means to assist guarantee your children are covered as cyclists can commonly cover multiple dependents simultaneously. When your child ages out of this insurance coverage, it might be possible to convert the biker into a brand-new plan.

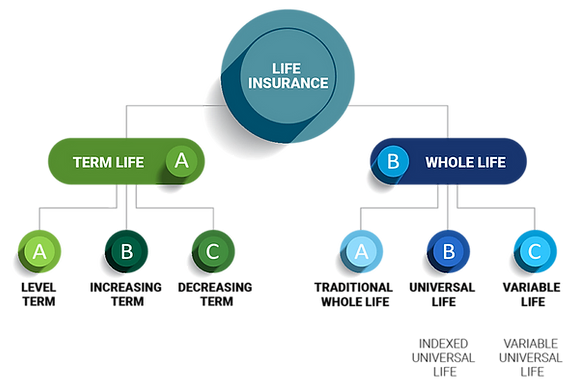

When comparing term versus long-term life insurance policy. the combination of whole life and term insurance is referred to as a family income policy, it is very important to bear in mind there are a couple of various types. One of the most usual kind of permanent life insurance policy is entire life insurance policy, but it has some essential distinctions compared to level term coverage. Below's a standard introduction of what to consider when contrasting term vs.

Entire life insurance coverage lasts permanently, while term protection lasts for a particular duration. The premiums for term life insurance policy are normally lower than whole life protection. Nevertheless, with both, the premiums stay the exact same throughout of the plan. Entire life insurance policy has a money worth part, where a part of the costs might expand tax-deferred for future requirements.

One of the primary features of degree term protection is that your costs and your fatality advantage do not change. You might have protection that starts with a fatality benefit of $10,000, which might cover a home loan, and after that each year, the fatality benefit will reduce by a collection amount or percent.

As a result of this, it's commonly a much more budget friendly sort of level term protection. You might have life insurance policy through your company, yet it might not suffice life insurance policy for your requirements. The very first step when acquiring a policy is figuring out exactly how much life insurance coverage you need. Consider elements such as: Age Household size and ages Employment condition Revenue Debt Lifestyle Expected final expenditures A life insurance policy calculator can help identify just how much you require to start.

After picking a plan, finish the application. For the underwriting process, you might have to give basic personal, health, way of life and employment information. Your insurance firm will certainly determine if you are insurable and the danger you may present to them, which is reflected in your premium expenses. If you're authorized, authorize the documentation and pay your first premium.

Effective Joint Term Life Insurance

Ultimately, think about scheduling time each year to review your plan. You might want to update your beneficiary details if you have actually had any considerable life adjustments, such as a marital relationship, birth or separation. Life insurance can in some cases really feel difficult. You do not have to go it alone. As you explore your alternatives, think about discussing your requirements, desires and worries about a financial specialist.

No, level term life insurance does not have money worth. Some life insurance plans have a financial investment attribute that enables you to develop cash money worth over time. A part of your costs repayments is alloted and can earn rate of interest in time, which grows tax-deferred throughout the life of your coverage.

You have some alternatives if you still want some life insurance protection. You can: If you're 65 and your coverage has run out, for example, you may desire to purchase a new 10-year degree term life insurance policy.

Premium Level Term Life Insurance Definition

You might have the ability to convert your term coverage right into a whole life plan that will last for the remainder of your life. Numerous kinds of level term plans are convertible. That suggests, at the end of your protection, you can convert some or all of your policy to entire life coverage.

Level term life insurance coverage is a policy that lasts a set term generally between 10 and 30 years and features a degree survivor benefit and degree premiums that stay the very same for the entire time the plan is in result. This indicates you'll know precisely just how much your payments are and when you'll have to make them, enabling you to budget plan as necessary.

Degree term can be an excellent alternative if you're looking to acquire life insurance policy coverage for the initial time. According to LIMRA's 2023 Insurance policy Barometer Research, 30% of all adults in the U.S. need life insurance coverage and do not have any kind of kind of policy yet. Level term life is foreseeable and cost effective, which makes it among one of the most prominent types of life insurance policy.

{kind=link}

Table of Contents

Latest Posts

Senior Care Funeral Insurance

Funeral Cover Benefits

Burial Insurance Prices

More

Latest Posts

Senior Care Funeral Insurance

Funeral Cover Benefits

Burial Insurance Prices